.svg)

.png)

At Esusu Identity Services (EIS), powered by Celeri, we often talk about the growing issue of fraud in the multifamily industry, particularly as it relates to falsified income documents. Fraudulent applicants submit modified pay stubs and bank statements — either edited themselves or even purchased online from sites that sell fake financial documents — to meet a property’s income requirements.

These bad actors are a leading driver of bad debt and costly evictions for multifamily operators, even when traditional screening still looks “clean” on the surface.

From our vantage point verifying thousands of documents every day, we wanted to share which income documents we see most frequently and which ones are most commonly modified.

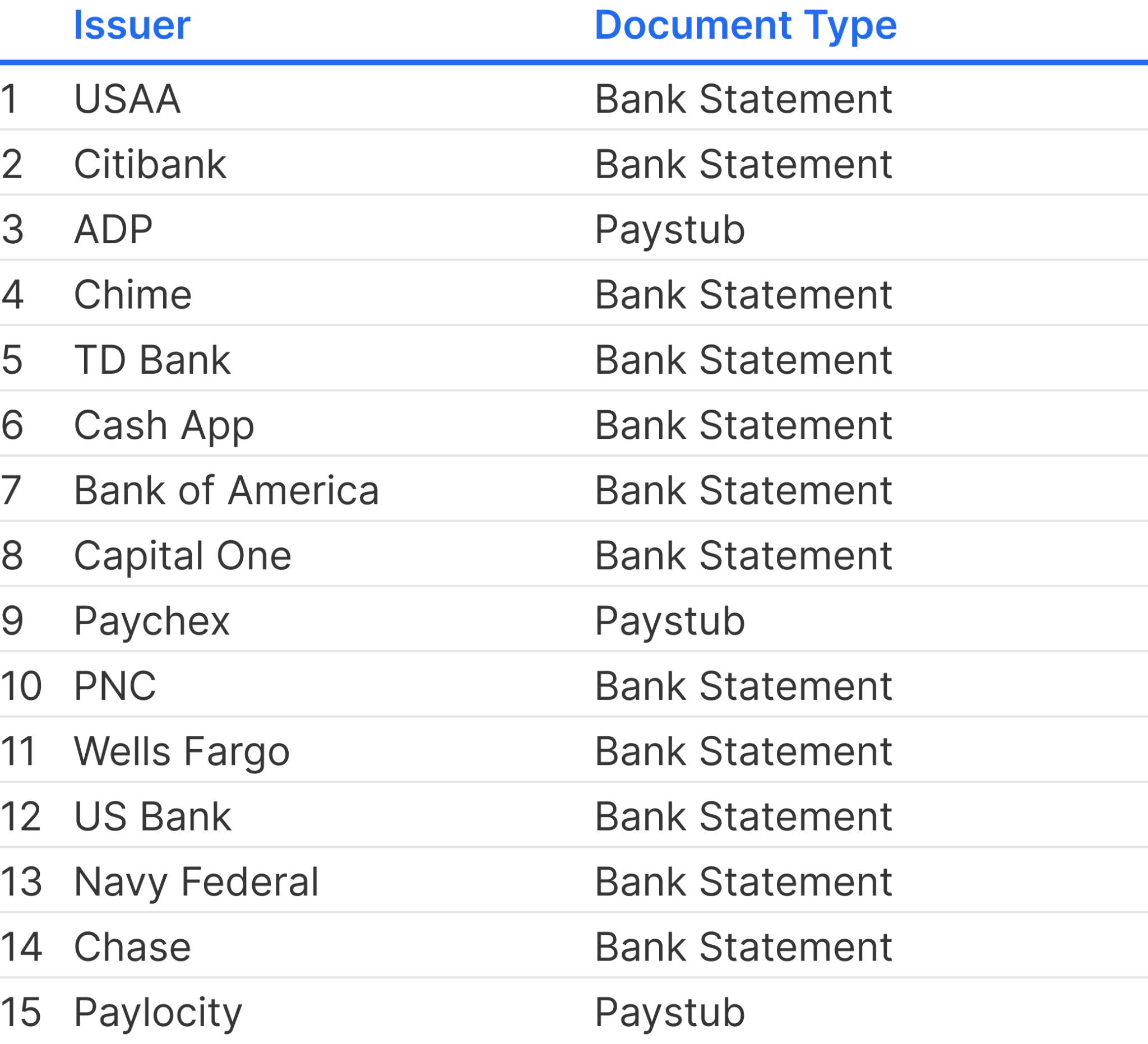

Most Commonly Received Income Documents

Across the country, we consistently see a similar pattern in the income documents submitted by rental applicants. As you’d expect, the list of issuers heavily features the largest financial institutions and payroll systems.

These typically include:

- Bank statements from major national and regional banks;

- Pay stubs from large payroll providers and in-house payroll systems;

- Other financial documents like benefit letters and portfolio statements in certain cases.

While the specifics vary by market and resident profile, the high-level pattern is clear: a relatively small group of issuers accounts for a large share of the documents that leasing teams see every day.

Income Documents With The Highest Rates of Fraud

Volume alone doesn’t tell the full story. Some issuers and document types are disproportionately targeted by fraudulent applicants, either because templates are easy to find online, or because the document format is simple to manipulate.

From our analysis, certain combinations of bank statements, pay stubs and common payroll providers show significantly higher fraud rates than the baseline.

This matters because fraud is not distributed evenly across all documents. Some documents are relatively low risk; others are repeatedly weaponized by bad actors who know how leasing teams are used to reviewing them.

Why This Matters For Multifamily Operators

The rise of falsified income documents creates real operational and financial risk:

- Approximately 1 in 10 rental applications include falsified income documents;

- Internal and industry data indicate that up to 50% of evictions stem from residents approved with fraudulent proof of income;

- Depending on the market, total eviction costs can range from $2,500 to $8,000 per case once you factor in lost rent, vacancy, legal fees, repairs, turnover, and leasing costs.

Each fraudulent approval is not just a single bad decision — it can become months of lost income, additional staff workload, and reputational risk.

Manual Review Alone is not Enough

Leasing teams are already stretched. Asking them to catch increasingly sophisticated fraud with only “eyeball review” creates several challenges:

- Edited PDFs and high-quality fakes are difficult to spot with the naked eye;

- Time spent manually scrutinizing documents slows down leasing velocity;

- Inconsistent review standards from associate to associate can introduce subjectivity and potential Fair Housing risk.

In practice, many teams end up in an uncomfortable middle ground: spending more time on review but still missing the most sophisticated fraud.

How Esusu Identity Services helps

Income Verification, delivered through Esusu Identity Services, is designed to give operators an objective, scalable way to validate income documents across their portfolios.

With Income Verification, operators can:

- Use AI-powered document analysis to detect edited or fabricated bank statements, pay stubs, and related financial documents;

- Match documents against real-world patterns to surface micro-anomalies and hidden edits that typical manual review may miss;

- Get results in seconds, so leasing teams can keep applications moving without compromising on risk.

Instead of relying on one-off checks for a handful of “suspicious” applicants, operators can:

- Standardize how income is verified;

- Apply consistent rules across properties and teams;

- Reduce the odds that a single fraudulent approval turns into months of delinquency and an expensive eviction process.

Turning document risk into a portfolio-level control

Knowing which income documents are most commonly modified is only the first step. The real value comes from turning those insights into repeatable controls:

- Build policies that require standardized sets of income documents from applicants;

- Use Esusu Identity Services to screen those documents consistently across your portfolio;

- Combine Income Verification with other Esusu tools, such as identity verification and rent reporting, to create a more complete risk and resident financial health strategy.

By doing so, operators can:

- Reduce bad debt driven by fraudulent move-ins;

- Decrease eviction-related losses;

- And free up leasing teams to focus on qualified applicants instead of document forensics.

What are you seeing in your applications?

If you’re starting to see patterns — certain pay stubs that “don’t feel right,” bank statements that seem off, or applicants who always have the same types of questionable documents — you’re not alone!

To learn more about:

- The income documents and issuers we see most frequently modified;

- How Esusu Identity Services (EIS) can help you standardize income verification across your portfolio.

Catching falsified income documents earlier in the process does more than protect NOI — it helps create a fairer, more consistent screening experience for honest applicants and onsite teams alike.