.svg)

What you need to know

- VantageScore 4.0 uses a 300-850 scoring range, where a good score falls between 661-780 (Prime), and 781-850 is considered excellent (Superprime).

- Renters with scores in the good range typically enjoy better approval odds for apartments, credit cards, auto loans, and mortgages, often with better interest rates and lower deposits.

- VantageScore 4.0 can incorporate rent payments when reported to the major credit bureaus, making platforms like Esusu valuable for renters building credit history.

- Improving a Vantage 4.0 score is gradual: consistent on time payments, keeping credit card balances low, and monitoring your credit report over months and years builds lasting progress.

What Is VantageScore 4.0 And How Does It Work?

VantageScore 4.0 is a credit scoring model launched in 2017 by VantageScore Solutions, a company created in partnership with Equifax, Experian, and TransUnion. Like VantageScore 3.0 and many FICO scores, it operates on a 300-850 scale, but with significant technological upgrades.

VantageScore 4.0 is the first credit scoring model to utilize trended data from all three major credit bureaus, allowing it to analyze consumer behavior over time rather than just a single point in time. The model incorporates trended data, analyzing up to two years of credit behavior patterns rather than just a snapshot, providing a more comprehensive view of financial habits.

VantageScore 4.0 utilizes advanced machine learning and trended data to be more predictive and inclusive than older models. Key improvements include:

- Reduced weight for certain public records;

- Exclusion of many medical collections from credit score calculations;

- Expanded ability to score people with limited credit histories.

When rent is reported to the credit bureau by platforms like Esusu, VantageScore 4.0 can use that payment history as part of its assessment — critical for renters who’ve been historically credit invisible.

What Is a Good VantageScore 4.0 Score?

A good VantageScore 4.0 score generally falls between 661 and 780. If you’re looking for the quick answer: scoring anywhere in this range puts you in what many lenders consider the “Prime” category, a solid position for financial opportunities.

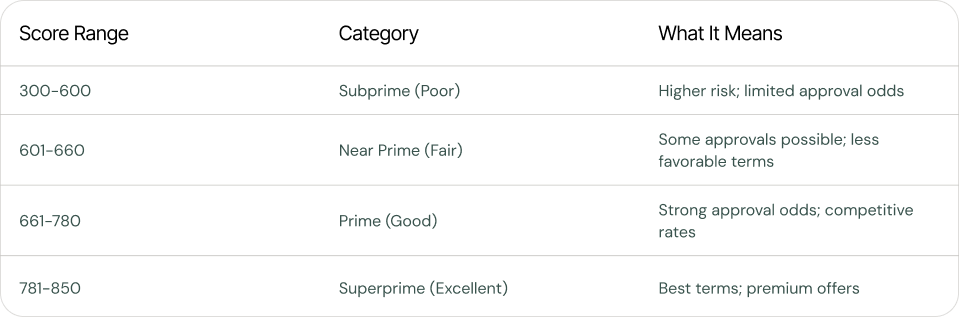

VantageScore 4.0 uses a 300-850 range. Here’s how the bands break down:

A VantageScore of 700 is generally considered a good credit score, landing comfortably within the good range defined as 661 to 780. For renters, reaching or maintaining this range can make qualifying for apartments, utilities, and everyday borrowing significantly easier.

VantageScore 4.0 Score Ranges And What They Mean

Understanding where you fall on the VantageScore 4.0 scale helps you know what to expect from lenders and property managers.

Subprime (300-600): Approval is challenging. When approved, expect higher interest rates and larger security deposits. Many lenders view this range as high risk.

Near Prime (601-660): Some approvals possible, but terms are typically less favorable. You may need additional documentation or higher deposits.

Prime/Good (661-780): This is where doors start opening. Approval odds improve significantly, interest rates become more competitive, and security deposit requirements often decrease.

Superprime/Excellent (781-850): The best rates and terms available. Financial institutions view you as very low risk.

As of early 2026, the average VantageScore 4.0 was roughly 701 — right in the good range. This benchmark helps you understand where you stand compared to other consumers.

Remember: lenders and property owners set their own cutoffs. A good score improves your odds but isn’t an automatic guarantee of approval.

.png)

Factors That Influence a Vantage 4.0 Score

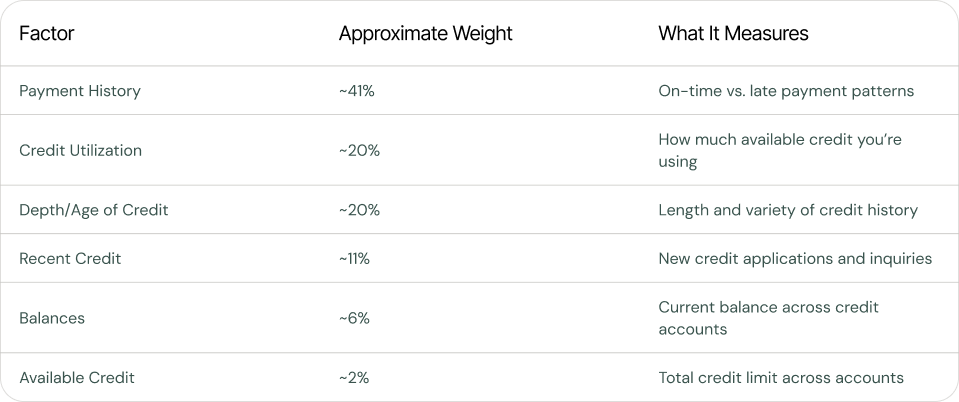

VantageScore 4.0 considers many of the same credit score factors as other scoring models but weighs them differently, especially payment history and recent credit behavior.

VantageScore 4.0 uses a scoring model that weighs payment history as the most significant factor, accounting for 41% of the score, while recent credit activity is weighted at 11%. Here’s the full breakdown:

Credit utilization measures how much of your revolving credit you use, ideally kept under 30%. For renters, this means keeping credit card balances well below your credit limit.

Importantly, personal characteristics like race, gender, income, and neighborhood are not used in VantageScore 4.0 calculations — aligning with financial inclusion principles.

How These Factors Show Up in Everyday Renter Life

Your daily financial behavior directly shapes your VantageScore 4.0. Here’s how:

- Paying rent on time feeds into payment history when reported through platforms like Esusu;

- Keeping your credit card under 30% of its limit supports healthy credit utilization;

- Avoiding three new store cards in one month prevents unnecessary credit inquiries;

- Maintaining that old no-fee card preserves your credit age and depth.

A missed rent payment or late payment on utilities, if reported, can negatively impact payment history. If you fall behind, catching up quickly matters — the sooner you’re current, the less lasting damage to your score.

What We See Among Renters

At Esusu, we see a pattern that drives our mission: many renters — especially those from historically marginalized communities — pay rent reliably every month but remain “thin-file” or credit invisible. They’ve demonstrated responsible financial behavior without receiving credit for it.

Esusu’s Rent Reporting solution helps renters build credit history by sending verified, on-time rent payments to the three major credit bureaus. Renters who consistently pay rent on time and participate in rent reporting often see stronger overall credit profiles over time, which can support healthier VantageScore 4.0 results.

We also provide property owners and operators with tools including analytics, flexible rent options, and resident financial health services that encourage more consistent on time payments.

Our mission centers on closing the racial wealth gap and expanding access to affordable credit through data-driven, inclusive rent reporting.

How Rent Reporting Fits Into VantageScore 4.0

VantageScore 4.0 can use rental tradelines when landlords or property managers report through platforms like Esusu to the credit bureau.

For renters with limited credit histories or no traditional credit, adding a positive rent tradeline may help establish a track record that VantageScore 4.0 can evaluate. The VantageScore 4.0 model is designed to score millions more consumers, including those with limited credit histories, by analyzing patterns of behavior over time — a significant advancement over previous models. If you are still building from the ground up, our guide on how to build credit with no credit history explains simple ways to start creating that track record.

Rent reporting supplements responsible use of other credit accounts. It’s one piece of building good credit, not a standalone solution. Results vary by individual profile.

.png)

What a “Good” VantageScore 4.0 Means in Real Life

A good VantageScore 4.0 in the 661-780 range translates to tangible everyday benefits.

For Renters:

- Higher approval odds for apartments without excessive documentation;

- Potentially lower security deposits;

- Better offers on credit cards with higher credit limits;

- Access to personal loan and auto loan options with better interest rates;

- VantageScore 4.0 allows for mortgage underwriting by Fannie Mae and Freddie Mac, meaning your score could help you qualify for homeownership.

For Property Owners:

- Residents with good consumer credit scores often correlate with improved collections;

- Lower delinquency rates reduce administrative burden;

- Stronger resident satisfaction and retention.

A good score doesn’t guarantee approval — lenders and landlords also evaluate income, debt-to-income ratio, employment stability, and other factors. But it significantly improves your position.

Good vs. Very Good vs. Excellent: Why Each Step Matters

Moving from good (661-780) to excellent (781-850) brings incremental benefits. Someone in the mid-600s might get approved but pay higher interest rates or deposits. Someone in the mid-700s typically sees more premium offers and a lower interest rate on loans.

From Esusu’s coaching perspective, the goal is steady progress — moving from fair to good, then from good to very good — rather than chasing a perfect 850. Even small improvements in your Vantage 4.0 score can open doors and reduce borrowing costs over time.

How Renters Can Work Toward a Good VantageScore 4.0

Anyone can take steps toward a good score, regardless of starting point. Here’s how to build credit responsibly:

- Pay all bills on time: rent, credit cards, loans, utilities. Set up autopay or calendar reminders.

- Keep credit utilization under 30%: if your credit limit is $1,000, keep your current balance under $300.

- Avoid opening several new accounts in a short period: space out credit applications by several months.

- Pay down existing debt over time: paying more than the minimum payment accelerates progress in repaying debt.

- Review your credit report regularly: check for errors and dispute inaccuracies through each credit bureau.

- Enroll in rent reporting: if your property partners with Esusu, ensure your on-time rent payments appear in your credit data.

Building or rebuilding credit with VantageScore 4.0 usually takes months and years, not days. Consistency in paying bills and maintaining healthy financial habits matters more than quick fixes.

Progress Over Perfection: Setting Realistic Credit Goals

Credit improvement is a journey with small, achievable milestones: moving from “no score” to “fair,” then into “good.” Track your progress over time, remembering that different sites may show different credit scores than Vantage 4.0 — VantageScore 3.0 and 4.0 may appear alongside many different credit scores and other scoring models.

Life happens — job loss, medical bills, unexpected expenses. One setback doesn’t define your financial future. Esusu’s broader resident financial health tools, like coaching and educational resources, support renters through these ups and downs.

How Property Owners and Managers Can Support Residents’ Vantage 4.0 Scores

Property owners and managers: resident credit health directly impacts occupancy, collections, and community stability.

Offering rent reporting through Esusu helps residents translate on-time rent payments into credit history that VantageScore 4.0 can use. This newer model can evaluate many lenders’ lending decisions more accurately when rent data is included.

Complementary tools Esusu provides include:

- Identity and fraud prevention;

- Analytics on rent payment trends;

- Flexible rent payment options that reduce delinquencies.

Communicate clearly with residents about how rent reporting works — participation is designed to help but doesn’t guarantee specific score changes. Position rent reporting as a resident benefit and ESG-aligned initiative supporting financial inclusion.

.png)

Monitoring and Understanding Your VantageScore 4.0

Not every app or bank shows VantageScore 4.0 — many still display VantageScore 3.0 or a FICO score. However, trends across multiple credit scores usually move in the same direction when you practice good financial behavior.

Check your credit scores and credit report regularly using legitimate sources. This helps you spot errors or fraud and understand how habits affect your profile. Credit scoring companies like VantageScore and FICO produce different credit scores — credit card issuers often provide free access to one or more.

Understanding inquiries: checking your own credit score is typically a soft inquiry that doesn’t affect your score. Hard credit inquiries from new credit applications may temporarily lower it.

Look beyond the number — review what’s on your credit report (revolving accounts, limits, balances, payment history) to understand which behaviors to adjust. Pairing regular monitoring with Esusu rent reporting and consistent on time payments supports a healthier trajectory.

Important Disclaimer About Credit Scores and Esusu

VantageScore 4.0 scores are calculated by VantageScore’s models using additional data supplied by the credit bureaus. Neither Esusu nor property owners set or control the score itself.

Individual results vary. The impact of any action — enrolling in rent reporting, paying down a card, disputing an error — depends on your overall credit profile and unique characteristics.

Esusu does not guarantee any specific credit score increase, approval for any loan or rental, or particular interest rate. Industry specific scores and different credit scores may also apply in various contexts.

Use this article for educational purposes. Consult official resources, nonprofit credit counselors, or financial professionals for advice tailored to your situation.

Working Toward and Maintaining a Good Vantage 4.0 Score

A good VantageScore credit score generally means 661-780, with 781-850 considered excellent. These ranges unlock better financial opportunities, from apartment approvals to mortgage access with favorable terms.

Consistent on time payments (including rent when reported), low credit utilization, and avoiding unnecessary new credit are the core habits supporting a good vantagescore. VantageScore 4.0 has revised how certain negative entries are considered, such as excluding medical debt and collections, which can positively impact scores for many consumers.

Esusu stands as a partner for renters and property owners who want to turn on-time rent into a credit-building asset. We’re here to strengthen financial health and resilience in communities nationwide.

Renters: Explore rent reporting options at your property or ask your property manager about Esusu. Property owners: Schedule a demo to learn how rent reporting can benefit your community.